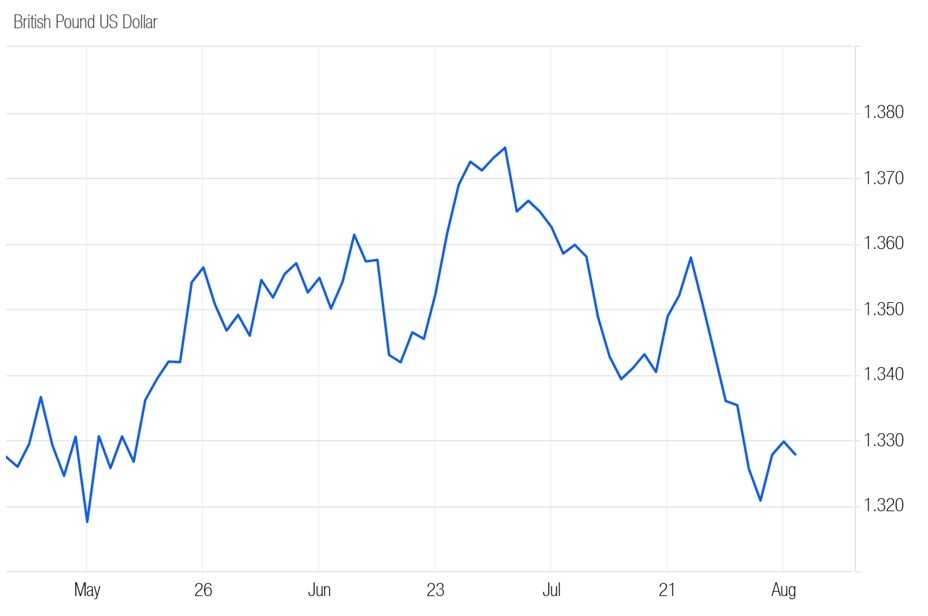

GBP/USD exchange rate suffers deep losses in July

The pound dollar exchange rate plummeted below 1.36 on 2 July as US employment figures supported market expectations of a Federal Reserve interest rate cut, while a selloff in British government bonds undermined the pound.

Having recovered slightly, the pair dropped around 1% into the 1.35 mid-range on 8 July after the Office for Budget Responsibility’s (OBR) latest fiscal risks report stoked concerns about the UK deficit.

The pound dipped below the 1.35 against the dollar on 11 July after disappointing GDP data showed the UK economy shrank for a second month in a row, contracting by 0.1% in May – a surprise drop that fuelled Bank of England (BoE) rate cut bets.

The pound was pressured by dovish signals from BoE governor Andrew Bailey, before hitting a three-week low in the 1.33 range on 15 July after US inflation rose to its highest level since February – prompting markets to trim bets on Federal Reserve interest rate cuts.

The pound dollar rate edged above the 1.34 benchmark the following day after official data showed UK inflation rose to a hotter-than-expected 3.6% in June after reaching 3.4% in May, prompting investors to scale back BoE rate cut bets.

Having climbed into the 1.34 mid-range amid dollar weakness, the pound was undermined by ongoing UK fiscal jitters on 18 July. Growing concern about UK debt led investors to speculate how much Chancellor Rachel Reeves may raise taxes in the Autumn.

The pound dollar rate climbed to a one-week high above 1.35 on 21 July as investors reduced bets for future BoE interest rate cuts, with analysts forecasting only one more reduction in 2025.

Meanwhile, the dollar was dented by persistent concerns over the future independence of the Federal Reserve, with Donald Trump continuing to pressure the US central bank to lower rates.

The pound rose to 1.358 on 23 July amid dollar weakness as markets digested the new US-Japan trade deal. While dollar investors welcomed the agreement, the resulting risk-on flows, coupled with Donald Trump’s continued criticism of Federal Reserve Chair Jerome Powell, weighed on the US currency.

The pound was pressured by lacklustre PMI data on 24 July showing a surprise deceleration in activity in the UK’s powerhouse service sector. Investors were also deterred from the UK currency by the uptick in job losses across the sector, stoking speculation that the BoE may action further interest rate cuts.

The pound faced further headwinds the following day after UK retail sales underwhelmed, causing it to slip to around 1.342 versus the dollar. While June’s results reflected a recovery following May’s significant downturn, the improvement fell short of expectations, resulting in continued pressure on the currency.

The pound dollar rate slumped into the 1.33 mid-range on 28 July after the US currency was bolstered by relief over the announcement of a long-awaited EU-US trade agreement. The dollar received additional support from increasing expectations that the Federal Reserve may sustain higher interest rates for an extended period, following recent strong US data.

The pair tumbled more than 1% to around 1.323 on 30 July after the dollar was supported by an encouraging GDP print that indicated a stronger recovery in the US economy. These gains were reinforced by the Federal Reserve’s decision to leave interest rates unchanged and Fed Chair Jerome Powell’s accompanying comments that favoured a tighter policy stance.

The pound dollar exchange rate ended the month at around 1.321 as lingering concerns about the UK’s fiscal credibility and a hotter-than-expected core PCE price index – the Fed’s favoured inflation gauge – in June applied further pressure.

GBPUSD: 3-Month Chart

Looking ahead

Markets were pricing in a BoE rate cut on 7 August before UK inflation data for June came in hotter-than-expected, dampening expectations of policy loosening – but only slightly.

Influential data from the UK economy in August: ILO Unemployment Rate (12 August), GDP (14 August), Consumer Price Index (20 August), S&P Global Composite PMI (21 August), Retail Sales (22 August).

Influential data from the US economy in August: Nonfarm Payrolls (1 August), ISM Services PMI (4 August), Consumer Price Index (12 August), Producer Price Index ex Food & Energy (14 August), Retail Sales (15 August), Michigan Consumer Sentiment Index (15 August), S&P Global Composite PMI (21 August), GDP (28 August), Core Personal Consumption Expenditures – Price Index (29 August).