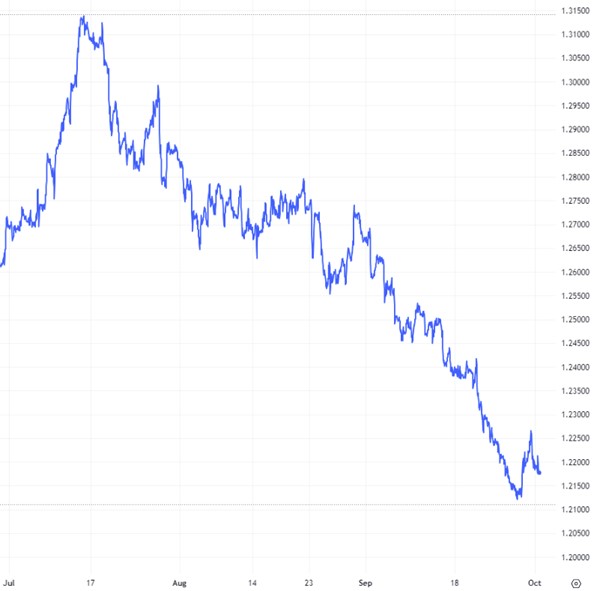

GBP-USD Exchange Rate Slumps to 6-Month Low in September

The tone was set for the month when the pound cratered against the dollar on 1 September after the latest non-farm payrolls data printed above forecasts, showing more jobs were created in the US in August than initially expected – pulling the GBP-USD pair below the 1.26 benchmark.

UK recession headwinds increased in force on 5 September following confirmation of a contraction in the service sector. The downbeat news stoked expectations that a significant, widespread, and prolonged downturn in economic activity is on the horizon – causing the pound to slip to the 1.25 mid-range against the dollar.

The GBP-USD pair’s downward spiral saw it fall into the 1.24 range the following day – a three-month low – after strong US economic data increased bets on further policy tightening from the Federal Reserve. The latest ISM services PMI showed business activity unexpectedly accelerated to a six-month high in August.

The pound struggled to buck its downward trend after the Recruitment and Employment Confederation (REC) published its latest survey which revealed the UK labour market is cooling.

The UK experienced a brief respite from the flagging economy following a cooldown in US core inflation. CPI data released on 13 September showed that while US headline inflation exceeded expectations, the gauge which ignores volatile products like fuel cooled significantly – causing investors to scale back bets on additional interest rate hikes from the Fed.

Lingering signs of labour market lethargy were exacerbated by a larger-than-forecast contraction in the British economy in July. The GDP print prompted renewed recession fears that dampened bets on more Bank of England (BoE) interest rate hikes – causing the pound to slump to a fresh three-month low on 14 September.

The dollar firmed on 20 September after Fed policymakers voted to keep interest rates on hold – an outcome that had been widely forecast. An optimistic tone in the central bank’s accompanying statement lent the US currency further support, as the FOMC expressed its determination to bring inflation to its 2% target while avoiding a recession.

Having traversed the 1.23 range, the GBP-USD pair crashed to a five-month low in the 1.22 mid-range following the BoE’s decision to keep rates on hold at 5.25%. Despite dissipating fears of higher borrowing costs, the central bank’s decision reflected ongoing economic concerns.

Following weaker inflation and a dovish BoE decision, the pound was dealt another chastening blow by the latest UK services PMI, which provided further evidence of a deepening contraction in the powerhouse sector – sparking another pound selloff that dragged it to a six-month low below the 1.22 benchmark against the dollar.

The risk-sensitive pound’s attempts to trim its losses against the dollar amid an improving market mood that dampened the safe-haven US currency were capped by the worrying economic data.

The UK currency fell to a fresh six-month low against a strengthening dollar on 27 September as markets priced in that the BoE has finished hiking interest rates as the economy deteriorates, while British inflation subsides.

The pound was set for its deepest monthly drop since August 2022, down more than 4% in September, as money markets re-evaluate the BoE’s rate outlook. Economists also expect the central bank to start cutting rates next summer.

GBPUSD: 3-Month Chart

Looking ahead

A fallow month in terms of interest rate decisions on both sides of the Atlantic means economic data will be in sharp focus for investors in the pound and the dollar in October.

Influential data from the UK economy in October: Claimant Count Change (17 October), Employment Change (17 October), ILO Unemployment Rate (17 October), Consumer Price Index (18 October), Retail Sales (20 October), S&P Global/CIPS Composite PMI (24 October).

Influential data from the US economy in October: ISM Manufacturing PMI (2 October), ADP Employment Change (4 October), ISM Services PMI (4 October), Average Hourly Earnings (6 October), Non-farm Payrolls (6 October), Producer Price Index ex Food & Energy (11 October), FOMC Meeting Minutes (11 October), Consumer Price Index (12 October), Retail Sales (17 October), S&P Global Services PMI (24 October), S&P Global Manufacturing PMI (24 October), Gross Domestic Product Annualized(Q3) (26 October).