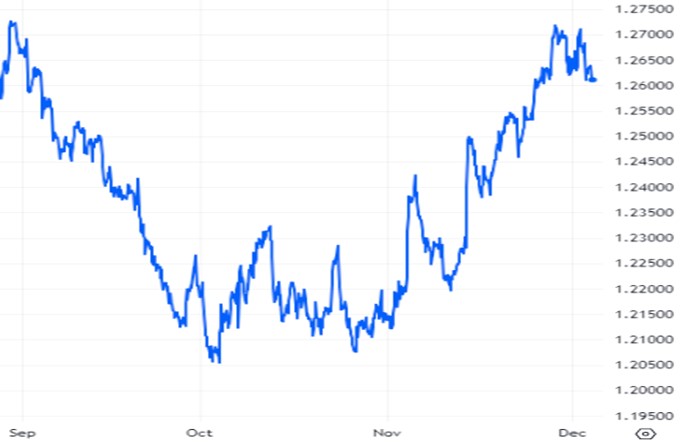

GBP-USD Exchange Charts an Upward Course in November

Interest rate announcements on both sides of the Atlantic at the start of November had similar outcomes but differing impacts on the GBP-USD pair.

The dollar was relatively unmoved by the Federal Reserve’s decision to extend its policy tightening pause, which kept a target interest rate of between 5.25% to 5.5% in its forecasts – suggesting a future hike is possible, although investors appeared unconvinced.

The following day, the Bank of England (BoE) elected to keep borrowing costs at a 15-year high, before ruling out the prospect of imminent rate cuts – causing the pound to strengthen.

According to BoE Governor Andrew Bailey: “Higher interest rates are working, and inflation is falling. But we need to see inflation continuing to fall all the way to our 2% target. We’ve held rates unchanged this month, but we will be watching closely to see if further rate increases are needed.”

The pound struck a two-month high against the dollar on 3 November following a woeful US non-farm payrolls pint for October, which came in significantly below forecasts – solidifying investor expectations that the Fed had concluded its aggressive tightening cycle.

As the dollar cratered in the wake of the news, the pound climbed more than 1.5%, taking it to 1.2381.

The UK currency soon arrested its gains after weak UK housing data and dovish rhetoric from the BoE sapped its strength, and a souring market mood pushed investors towards the safe-haven dollar – causing it to slide to an eight-day low below the 1.22 level.

The pound shrugged off news that the UK economy had stagnated following the release of the UK’s latest GDP data on 10 November. Thankfully for the UK currency, it printed higher than expected, allowing the GBP-USD pair to remain rangebound.

Another surge in pound value was spurred by cooler-than-expected US inflation data that undermined the dollar on 14 November, while upbeat UK jobs data lent additional support – propelling it to a six-week high.

The pound retreated the following day as significant cooling in both headline and core UK inflation trimmed BoE rate hike expectations, with investors speculating that borrowing costs might have peaked.

As the pound licked its wounds, the dollar drifted higher amid US retail sales data which revealed signs of increased consumer spending. Meanwhile, the UK currency faced further headwinds following weaker-than-expected retail sales numbers released two days later.

The pound soon recovered to climb into the 1.25 midrange – an 11-week high – against the dollar on 21 November, following hawkish comments from BoE policymakers.

Governor Andrew Bailey cautioned that markets may be too optimistic regarding expectations for interest rate cuts. Meanwhile, fellow BoE rate-setter Catherine Mann categorically stated that she was in favour of further rate hikes.

Meanwhile, the dollar felt the weight of diminishing Fed interest rate expectations, prompting investors to raise bets on the central bank to start to loosen its monetary policy next year.

The following day the UK currency plummeted to the 1.24 midrange as Chancellor Jeremy Hunt used the Autumn Statement to announce an increase in business rates for larger firms.

What’s more, the Office for Budget Responsibility (OBR) downgraded its forecast for UK growth and employment – creating a damaging blend of disappointing fiscal policies and economic uncertainty for the pound.

Meanwhile, the dollar was given a shot in the arm by a far larger drop in US jobless claims than forecast – reigning in bets on Fed interest rate cuts.

The pound’s seesawing form continued when better-than-forecast UK PMI reports and thin US trading conditions allowed it to claw back its losses and reach a two-month high against the dollar. Crucially, November’s preliminary PMI figures revealed a surprise expansion in the UK’s vital services sector.

Having edged above the 1.26 level, the pound traversed the range amid an absence of UK data. Before breaking through 1.27 on 28 November for the first time since the end of August, as mounting bets on the Fed adopting a more accommodative policy stance next year sent the dollar into a tailspin.

GBPUSD: 3-Month Chart

Looking ahead

Speculation about rate cuts following the conclusion of the BoE’s next meeting of rate-setters on 14 December was given short shrift by Governor Bailey in November.

Influential data from the UK economy in December: Claimant Count Change (12 December), Consumer Price Index (13 December), Retail Sales (15 December), S&P Global/CIPS Composite PMI (20 December), GDP (22 December).

The Fed’s next policy announcement is scheduled for 13 December, with interest rates expected to remain unchanged at 5.25% to 5.5% amid cooling inflation.

Influential data from the US economy in December: ISM Manufacturing PMI (1 December), ISM Services PMI (5 December), ADP Employment Change (6 December), Nonfarm Payrolls (8 December), Consumer Price Index (12 December), Retail Sales (14 December), S&P Global Services PMI (18 December), GDP (21 December), Core Personal Consumption Expenditures – Price Index (22 December).