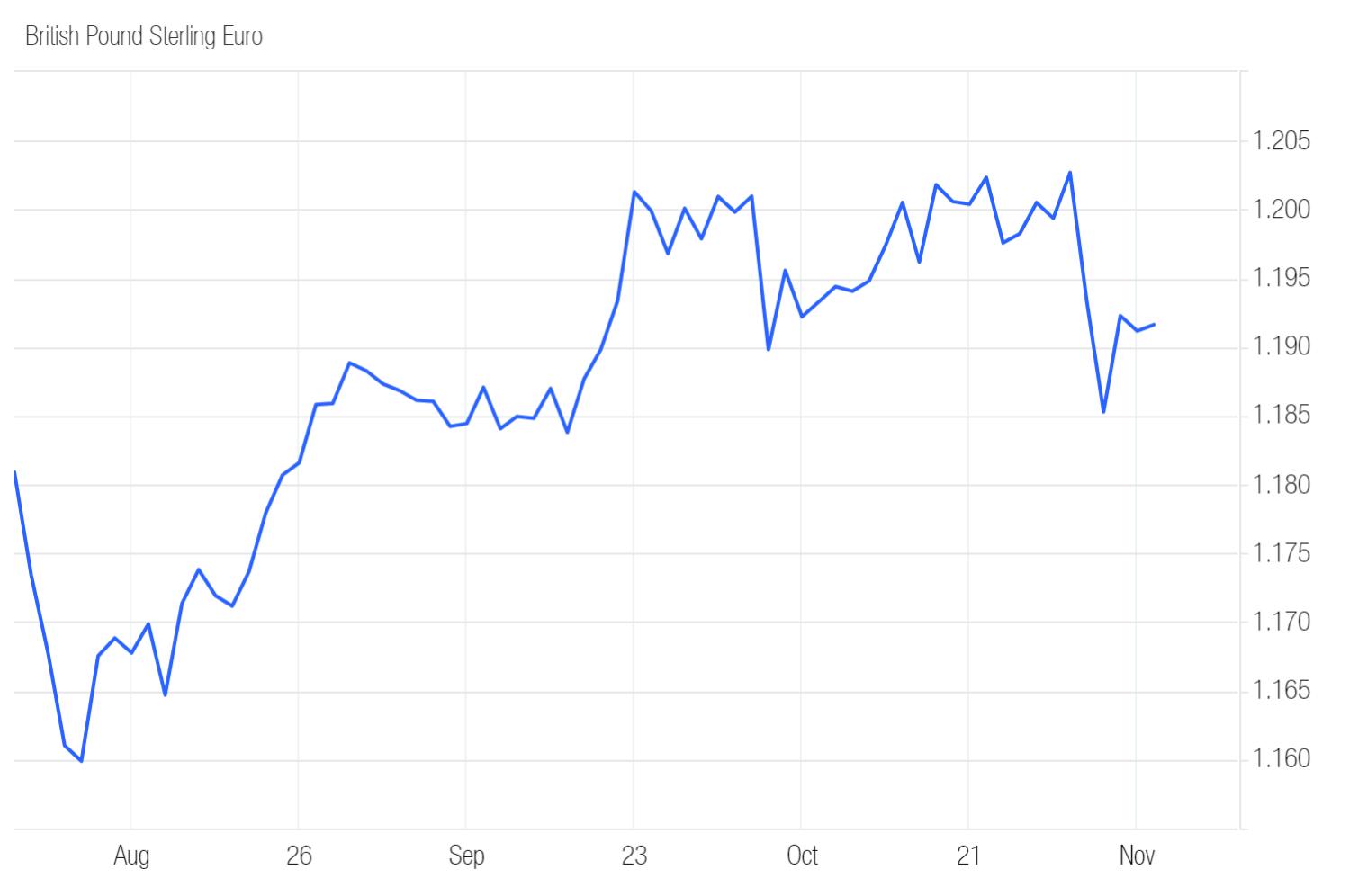

GBP/EUR exchange rate hits two-year high in October

The pound euro exchange rate nosedived by more than 1.1% into the €1.18 mid-range on 3 October – its lowest level since 20 September. The depreciation was prompted by remarks from Bank of England (BoE) Governor Andrew Bailey who indicated that further signs of easing inflation could spur the central bank to become “a bit more activist” in its approach to monetary policy. Meanwhile, the euro was supported by the latest Producer Price Index (PPI) figures from the Eurozone, which reported a monthly increase.

The pound rebounded from a two-week low the following day after the BoE’s Chief Economist Huw Pill cautioned against lowering interest rates too quickly, propelling the UK currency into the €1.19 mid-range.

Data released on 7 October reported that retail sales in the bloc rose 0.2% in August, jumping from July’s stagnant print, while German factory orders plunged 5.8%, marking their worst fall in seven months. The pound dropped to a fraction above €1.19 on the news.

A period of relative calm followed, despite better-than-expected German trade data and an upbeat UK GDP print, before the pound euro rate climbed above €1.20 on 15 October. The catalyst for movement was the latest UK jobs report which showed the rate of unemployment in the UK fell to 4% in August, down from 4.1% – its lowest since January. However, the pound’s gains were capped by wage growth which recorded another slowdown.

The pair’s upward trajectory was cut short the following day by the UK’s Consumer Price Index (CPI), which showed UK inflation printed below market expectations in September. Headline inflation fell to a three-year low of 1.7%, rather than a 1.9% expectation, while core inflation was 3.2%, taking it lower than economists’ expectations of 3.4%. The numbers opened the door for the BoE to cut interest rates further, causing the pound to slump more than 0.5% to around €1.193.

The pound retraced its losses on 17 October, rising a fraction above the €1.20 benchmark, after the European Central Bank (ECB) announced its first back-to-back interest rate cut since 2011 to thwart a sharp slowdown in the Eurozone economy – a move that undermined the single currency.

The pound euro rate touched a two-year high in the €1.20 mid-range the next day amid tailwinds generated by the ECB’s rate cut and mounting speculation that the central bank will race to unwind monetary policy further. Meanwhile, the pound was bolstered by UK retail sales which grew by 0.3% in September, defying forecasts that they would fall by 0.4%.

ECB President Christine Lagarde emphasised the need for a cautious, data-driven approach to further rate cuts on 23 October. With the euro buoyed by her comments, the pound dipped below €1.20.

The pound was initially muted on 24 October following the publication of lacklustre UK PMIs showing the indices for manufacturing and services both printed lower than expected but remained above the 50 threshold that separates expansion from contraction. However, the emergence of risk-on flows undermined the safe-haven euro allowing the increasingly risk-sensitive pound to climb above €1.20.

The pound euro rate returned to the €1.20 mid-range on 29 October amid a diverging Eurozone and UK monetary policy outlook, with interest rates projected to fall at a slower pace in the UK than the Eurozone.

The new Labour government delivered its first budget in 15 years on 30 October. As expected, UK Chancellor Rachel Reeves proposed a raft of tax rises to the tune of £40bn, which saw the pound slump to around €1.193. However, its downside was limited by an increase to UK borrowing which could fuel inflation and in turn prevent further BoE interest rate cuts. Meanwhile, the euro was bolstered by warmer-than-expected German inflation data and positive GDP readings from the Eurozone and Germany, with the latter skirting recession.

The pound extended its losses the following day, sinking to a four-week low in the €1.18 mid-range, amid mounting concerns over the huge tax and spending plans provided in the Autumn Budget. Meanwhile, the euro was supported by the Eurozone’s latest CPI which reported that both headline and core inflation printed above market forecasts, dampening ECB interest rate cut bets for December.

GBPEUR: 3-Month Chart

Looking ahead

Having held interest rates at 5% in September a further cut is expected at the next meeting of the BoE’s Monetary Policy Committee on 7 November following the sharper-than-expected drop in the September inflation figure – a move that is likely to weigh on the pound.

Influential data from the UK economy in November: ILO Unemployment Rate (12 November), Average Earnings Excluding Bonus (12 November), GDP (15 November), Consumer Price Index (20 November), Retail Sales (22 November), S&P Global/CIPS Services PMI (22 November).

The next ECB policy meeting is scheduled for 12 December. Therefore, investors will monitor economic indicators from the bloc in November that signal the likelihood of further rate cuts, such as the Eurozone CPI on 19 November and German GDP on 22 November.