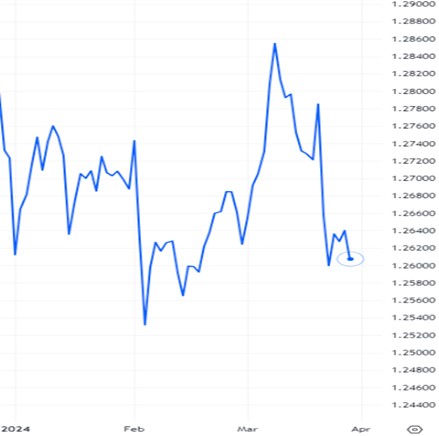

GBP-USD Exchange Rate Touches Seven-Month High in March

The GBP/USD exchange rate began to firm on 4 March – testing 1.27 – as Federal Reserve interest rate bets were stoked by an unexpected downturn in US manufacturing, which weighed on the dollar.

The pair’s upward momentum was checked on 6 March following the unveiling of the spring Budget. UK Chancellor Jeremy Hunt addressed Parliament to announce a raft of tax cuts designed to stimulate economic growth, such as the expected 2p cut to national insurance.

However, the Office for Budget Responsibility (OBR) forecast that UK inflation would drop below the Bank of England’s (BoE) 2% target within the next few months. The outlook bolstered rate cut bets, denting the pound.

The pound quickly shrugged off its post-budget hangover to break through 1.28 the following day amid heavy risk-on flows that undermined the safe-haven dollar.

The UK currency touched a seven-month high against the dollar on 8 March, rising for a sixth straight day to 1.2840, after data showed the US economy added 275,000 jobs in February, beating forecasts. Immediately following the influential nonfarm payrolls report, investors raised bets on faster and earlier interest rate cuts, which muddied the US currency’s appeal.

The pound’s sharp rise was blunted on 12 March in the wake of softer-than-expected UK employment data. The print showed average earnings excluding bonuses cooled and the unemployment rate unexpectedly crept up in the three months preceding January.

Meanwhile, the dollar advanced following the release of firmer-than-expected inflation data that slightly pared Fed rate cut bets. The US consumer price index (CPI) rose unexpectedly to 3.2% in February, compared with the estimated 3.1% rise.

The GBP/USD exchange rate tumbled into the 1.27 midrange on 14 March after key US data dampened expectations of early interest rate cuts – a hawkish view that bolstered the dollar. US producer prices rose by 0.6% in February from January, twice as fast as forecast. Retail sales in the US recovered by 0.6% following January’s surprise 1.1% decline, but economists had forecast a larger rebound of 0.8%.

Following a period of relative calm, the GBP/USD exchange rate slumped below 1.27 as UK inflation cooled to a two-and-a-half-year low. CPI data showed headline inflation dropped to 3.4% in February, rapidly decelerating from January’s 4%. Similarly, core inflation eased to 4.5%, below expectations of 4.6%. The numbers triggered a flurry of speculation that rapidly cooling consumer prices may lay the foundations for BoE summer interest rate cuts, souring pound sentiment.

The pound rebounded to within a whisker of the 1.28 benchmark after the Fed announced that it would leave US interest rates at a 25-year high as it continues to assess their impact on sticky inflation. The dollar was dealt a blow when the central bank used its accompanying statement to signal that it still expects to cut rates three times this year.

The UK currency soon tumbled from a weekly high on 21 March amid growing expectations that the BoE could fire the starting gun on its rate-cutting cycle in the second quarter of 2024. Having announced its decision to hold interest rates at 5.25%, the central bank revealed that its Monetary Policy Committee’s (MPC) more hawkish participants had moderated their policy view by voting to maintain the current base rate.

The pound dropped to a fresh monthly low against the dollar on 22 March in the upper reaches of the 1.25 range as investors continued to speculate over the BoE’s policy path. Governor, Andrew Bailey stated that rate cuts were “in play” at future MPC meetings.

Having traversed the 1.26 range, the pound was tripped up on 28 March by data confirming the UK entered a technical recession in the final six months of last year, causing the UK currency to stumble into 1.25 territory.

The GDP figures showed that the economy contracted by 0.1% in the three months between July and September, followed by a further 0.3% shrinkage in the fourth quarter (between September and December).

GBPUSD: 3-Month Chart

Looking ahead

A fallow month in both the BoE and Fed policy meeting calendars means rate-setters aren’t scheduled to gather until May on both sides of the Atlantic. This brings macroeconomic data into sharp focus for clues on the path of policy easing.

Influential data from the UK economy in April: ILO Unemployment Rate (16 April), Average Earnings (16 April), Consumer Price Index (17 April), Retail Sales (19 April), S&P Global/CIPS Services PMI (25 April).

Influential data from the US economy in April: ISM Manufacturing PMI (1 April), ADP Employment Change (3 April), ISM Services PMI (3 April), Nonfarm Payrolls (5 April), Consumer Price Index (10 April), FOMC Minutes (10 April), Producer Price Index ex Food & Energy (11 April), Michigan Consumer Sentiment Index (12 April), Retail Sales (15 April), S&P Global Manufacturing PMI (23 April), S&P Global Services PMI (23 April), Gross Domestic Product (25 April), Core Personal Consumption Expenditures – Price Index (26 April).