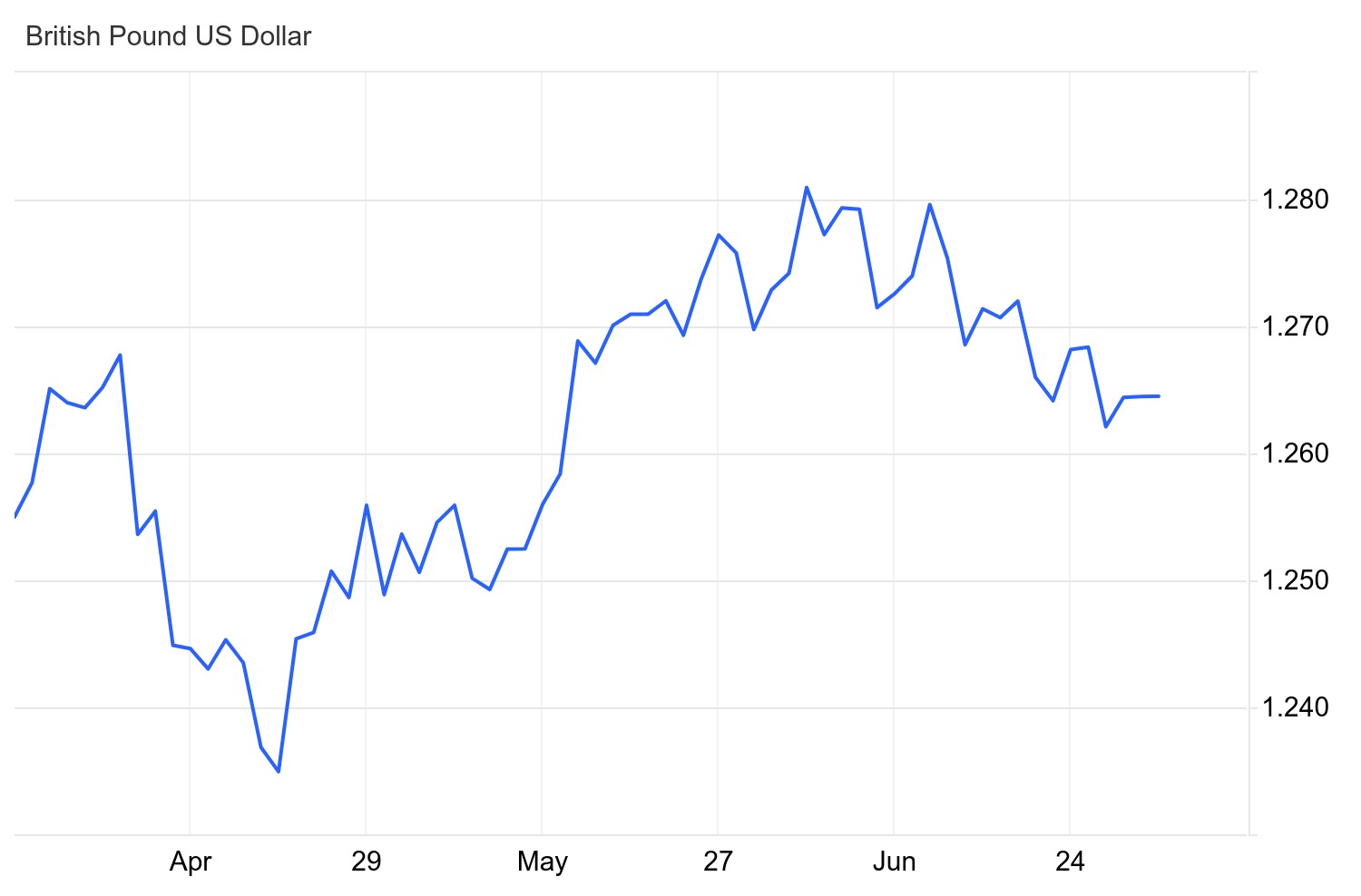

GBP-USD Exchange rate touches ten-month high in June

The pound dollar exchange rate bounced off the 1.27 benchmark on 3 June after the ISM manufacturing PMI showed a sharper-than-forecast contraction in US factory activity in May. This marked an unexpected fall in the PMI for a second consecutive month, causing the pair to rebound a fraction above 1.28.

The pound slumped to 1.272 versus the dollar on 7 June following the publication of US non-farm payrolls data for May that showed 272,000 jobs were added to the economy – significantly outstripping forecasts of 185,000. This sign of a robust economy stoked speculation that the Federal Reserve may only cut rates once this year.

Following a period of relative calm amid a data lull on both sides of the Atlantic, the pound hit a ten-month high against the dollar in the 1.28 mid-range on 12 June. A surprise cooldown in US headline inflation dented the dollar after the CPI decelerated to 3.3% in May, rather than holding at 3.4% as forecast. Markets subsequently began betting that the Fed would begin loosening its monetary policy sooner than expected.

This was quickly followed by the Fed’s interest rate decision as its June meeting of policymakers concluded. Although it kept rates on hold at 5.5% as expected, the accompanying press release revealed FOMC members are now pencilling in just one cut this year against a backdrop of persistent US inflation, down from a previous estimate of three. The hawkish U-turn allowed the dollar to regain a chunk of its losses.

The pound dollar exchange rate nosedived below the 1.27 benchmark on 14 June amid a politically charged risk-off mood in markets that allowed the safe-haven US currency to firm.

The pound wavered near a monthly low around 1.266 against the dollar on 17 June amid a lack of fresh trading impetus.

Having clawed back above the 1.127 benchmark, the pound dollar rate retreated following the publication of the latest UK CPI, which showed headline inflation cooled to the Bank of England’s (BoE) 2% target for the first time in three years – rekindling rate cut speculation that pressured the UK currency.

This was swiftly followed by the BoE’s June policy announcement on 20 June. Central bank rate-setters enacted a widely anticipated hold in interest rates accompanied by dovish forward guidance that reinforced rate cut speculation and dented the pound further.

The UK currency extended its losses the following day in the face of robust US data that supported the dollar. In June, both US manufacturing and services PMIs printed above forecasts and reflected expansion in the sectors, causing the pound dollar rate to bottom out at 1.262.

While the pound received a modicum of support from the latest UK retail sales data, the preliminary PMIs for June offset this. In May, retail sales printed well above expectations, while June’s PMIs proved mixed, with the UK’s manufacturing index ticking higher and the services index falling, signalling slowing economic activity.

The pound began edging higher on 24 June amid an increasing appetite for risk that undermined the safe-haven dollar, before sliding back to 1.262 two days later as economic tensions intensified ahead of the UK’s general election.

The pound dollar rate firmed slightly as June drew to a close after news of cooling US inflation undermined the dollar. The pair ended the month at 1.265.

GBPUSD: 3-Month Chart

Looking ahead

The next BoE interest rate decision is scheduled for August, so investor attention will be fixed on inflation figures for June on 17 July.

Influential data from the UK economy in July: Gross Domestic Product (11 July), Consumer Price Index (17 July), ILO Unemployment Rate (18 July), Retail Sales (19 July), S&P Global/CIPS Composite (23 July).

Market analysts think it’s a long shot, but the Fed could enact its first interest rate cut on 31 July as recessionary cracks start to form in the economy. However, most analysts expect the first cut to happen in either September or November.

Influential data from the US economy in July: ISM Manufacturing PMI (1 July), ADP Employment Change (3 July), ISM Services PMI (3 July), Nonfarm Payrolls (5 July), Consumer Price Index (11 July), Producer Price Index excluding Food & Energy (12 July), Retail Sales (16 July), S&P Global Composite PMI (23 July), Gross Domestic Product (25 July), Core Personal Consumption Expenditures – Price Index (26 July), ADP Employment Change (31 July).