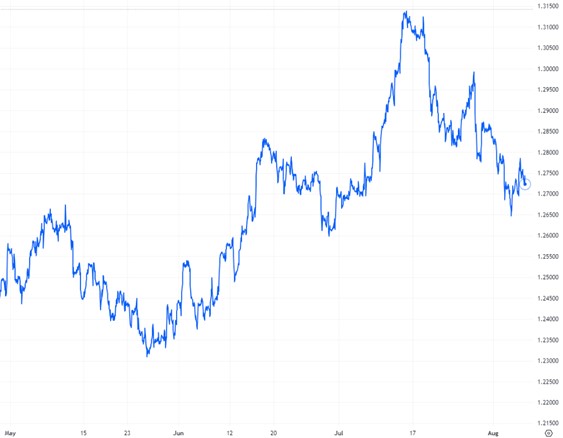

GBP-USD Exchange Rate Hits 15-Month High in July

A lack of major economic data left the pound exposed to market sentiment and economic uncertainty in early July – troubling conditions that were exacerbated by investor concerns that relentless policy tightening could tip the UK into a recession.

Despite this precarious position, the UK currency appeared sanguine. It rallied against the dollar amid economists’ expectations that the US economy will cool by the end of the year, despite the prospect of further tightening – lifting the pound into the 1.27 range.

The US policy outlook was supported by the publication of hawkish Federal Open Market Committee (FOMC) minutes on 5 July, which revealed almost all rate-setters favoured a return to hiking rates after the latest pause. The minutes stated: “Almost all participants noted that in their economic projections that they judged that additional increases in the target federal funds rate during 2023 would be appropriate.”

The GBP-USD rate jumped above the 1.28 benchmark – a 14-month high – after the latest US non-farm payrolls report fell short of expectations on 7 July. The US economy added 209,000 jobs in June, missing forecasts of 225,000. Additionally, May’s job creation print was revised down from 339,000 to 306,000.

The pair consolidated in the 1.28 range before more data-fuelled tailwinds propelled it higher. A combination of softening US inflation and red-hot UK wage growth that supported expectations of more tightening from the Bank of England (BoE) helped it break through 1.31 to reach a 15-month high on 14 July.

Having jumped almost 2% in seven days the pound took a breather, sustaining its gains against the dollar until 19 July when lower-than-expected CPI figures from the UK economy caused it to slip into the 1.28 mid-range by 21 July.

Data published by the ONS showed headline inflation decelerated from 8.7% to 7.9% in June – below the 8.2% cool down that was forecast.

The inflation reading was cited by analysts as a potential “turning point” in the UK’s battle against inflation. While the BoE is still some way off returning inflation to its 2% target, investors in the pound hoped June’s figures will allow the UK central bank to take its foot off the policy pedal slightly.

The pound’s move lower was accelerated by stronger-than-expected initial jobless claims data from the US economy, with the number of Americans filing for unemployment benefits tumbling by 9,000 from the previous week – the lowest level in two months. The dollar rallied on the news with investors placing bets on further tightening from the Federal Reserve amid a stubbornly tight US labour market.

Better-than-expected retail sales helped the pound to right itself. The ONS reported that the hottest June on record boosted sales, which increased 0.7% against expectations of a modest increase of 0.2% month-on-month.

The GBP-USD rate remained steady as the market braced for the Fed rate decision on 26 July, before rallying after the FOMC hiked borrowing costs by 25bps to 5.5% – a new 22-year high.

Speaking in his accompanying press conference, Fed Chair Jerome Powell’s dovish tone took investors by surprise after he suggested any further tightening of monetary policy would be data dependent.

His non-committal outlook for a September rate hike propelled the pound as much as 0.4% higher against the dollar to strike highs of 1.2950.

GBPUSD: 3-Month Chart

Looking ahead

The BoE raised interest rates to 5% in June – despite ebbing inflation – and is expected to increase them again to 5.25% in August, with the UK central bank announcing its decision on 3 August.

Influential data from the UK economy in August: Gross Domestic Product (11 August), Claimant Count Change (15 August), ILO Unemployment Rate (15 August), Consumer Price Index (16 August), Retail Sales (18 August), S&P Global/CIPS Composite PMI (23 August).

Influential data from the US economy in August: ISM Manufacturing PMI (1 August), ADP Employment Change (2 August), ISM Services PMI (3 August), Nonfarm Payrolls (4 August), Consumer Price Index (10 August), Producer Price Index excluding Food & Energy (11 August), Retail Sales (15 August), FOMC Minutes (16 August), S&P Global Manufacturing and Services PMIs (23 August), Gross Domestic Product (24 August).