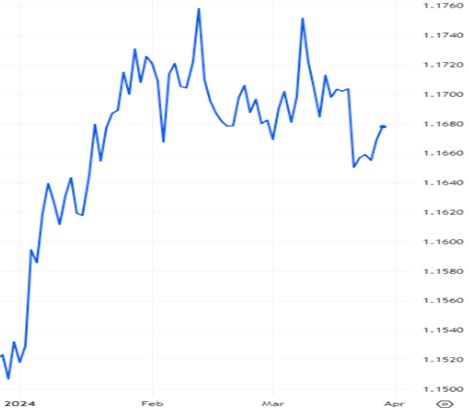

GBP-EUR Exchange Rate Falls to Nine-Week Low in March

The GBP/EUR exchange rate traded sideways in the 1.16 range at the start of the month, despite warmer-than-forecast Eurozone inflation data that reinforced speculation that interest rates could remain higher for longer in the bloc to cool sicky inflation.

Bank of England (BoE) chief economist Huw Pill indicated the central bank is still “some way off” cutting interest rates – hawkish comments that helped to support the pound.

The pair began edging higher on 4 March ahead of the spring Budget and the European Central Bank’s (ECB) interest rate decision.

The pound retraced its marginal gains, dropping just below 1.17, following the delivery of a Budget that sprung few surprises. Having explained that the economy is forecast to grow by 0.8% this year after falling into a recession at the end of last year, the Chancellor announced a slew of tax cuts.

The pound struck a three-week high just above 1.17 against the euro as investors digested the ECB interest rate decision on 7 March. While the central bank kept rates steady as expected, and provided few clues about policy loosening, it revised its inflation forecasts lower – prompting rate cut bets that soured euro sentiment.

A fresh three-week high in the 1.17 mid-range the next day was achieved despite upbeat data from the embattled German economy – the largest in the single currency area. The euro’s upside potential was capped in the wake of dovish interest rate expectations in the bloc following the ECB’s inflation forecast.

The GBP/EUR exchange rate began sliding lower on 11 March amid a lack of key data from both the UK and the Eurozone, with the euro supported by a risk-on mood in markets.

The pair remained on the back foot the next day following an unexpected increase in UK unemployment, causing it to dip below 1.17. The number of people out of work unexpectedly increased in the three months to January, while average earnings (excluding bonuses) surprised investors by cooling – stoking BoE rate cut speculation that weighed on the pound.

Signs of improving UK economic activity couldn’t inspire the pound. January GDP data printed in line with forecasts, posting 0.2% growth. The reading, and future forecasts, point to a mild recession that won’t drag on.

The euro managed to shrug off news that industrial production in the Eurozone tanked by an unexpected 3.2%, well below forecasts of 1.5%. This level marked the worst deterioration in activity since March 2023, sullying the bloc’s economic outlook.

The pound edged higher against the euro on 14 March on the back of rate cut chatter from ECB policymaker Yannis Stournaras: “We need to start cutting rates soon so that our monetary policy does not become too restrictive. It is appropriate to do two rate cuts before the summer break, and four moves throughout the year seem reasonable.”

The GBP/EUR exchange rate remained flat on 18 March amid confirmation of cooling headline inflation in the bloc that’s creeping towards the ECB’s 2% target. With the pound experiencing a data lull, the euro managed to resist the downward pressure from increased rate cut bets.

A sharp fall in UK inflation exposed the pound to pressure on 20 March, as it appeared to open the door to BoE rate cuts this summer. In February, the UK’s headline consumer price index eased to 3.4%, below forecasts of a drop to 3.5% – its lowest level for two and a half years.

The pound’s woes were compounded the next day after the BoE announced its fifth consecutive interest rate hold, which ramped up policy-loosening expectations.

Sluggish UK retail sales were the straw that broke the camel’s back on 22 March, sending the pound to a nine-week low just above the 1.16 level. Retail sales volumes remained unchanged in February from the previous month’s upwardly revised 3.6% increase.

The GBP/EUR exchange rate was rangebound during the last week of March despite upbeat UK retail data, improving German consumer confidence and dovish ECB remarks.

GBPEUR: 3-Month Chart

Looking ahead

The next BoE policy meeting is scheduled for May, bringing macroeconomic data into sharp focus in April for clues on the path of policy-easing.

Influential data from the UK economy in April: ILO Unemployment Rate (16 April), Average Earnings (16 April), Consumer Price Index (17 April), Retail Sales (19 April), S&P Global/CIPS Services PMI (25 April).

The next ECB policy meeting takes place on 11 April. The central bank is expected to keep interest rates on hold, before potentially firing the starting gun on its rate-cutting cycle in June.