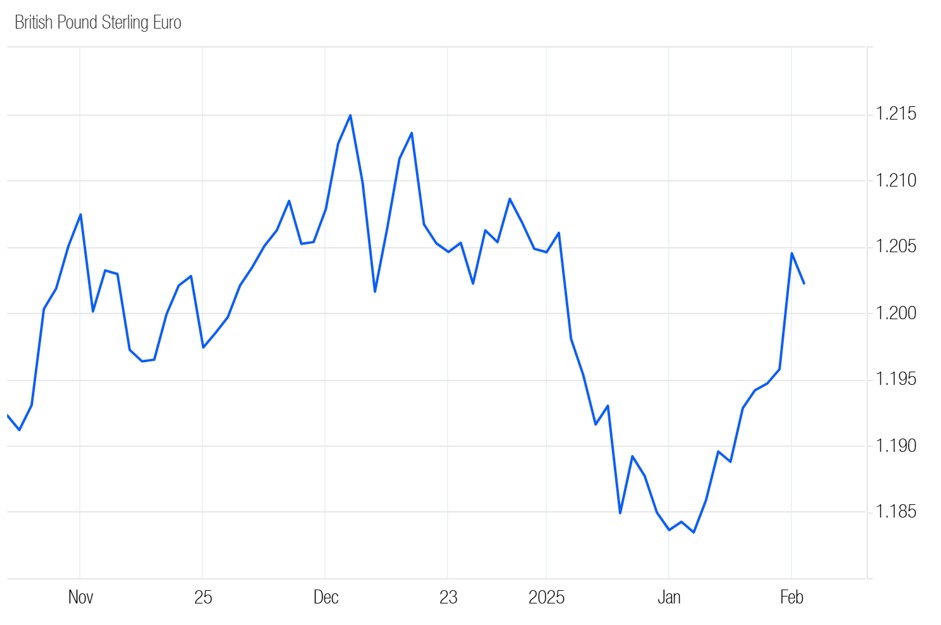

GBP/EUR exchange rate falls to 5-month low in January

The pound traversed the €1.20 mid-range versus the euro before tumbling to around €1.19 on 8 January amid mounting concerns about the impact of climbing UK bond yields on public finances.

Pound headwinds increased the following day as the UK bond market selloff intensified. Worries of low growth and higher debt deterred investors from the UK, causing it to dip to around €1.191 – a 10-week low.

The pound euro exchange rate touched a fresh two-and-a-half-month low on 13 February as UK government borrowing costs continued to climb.

The pair slid into the €1.18 mid-range on 14 February, extending its multi-month lows, as worries the UK government will be forced to make further spending cuts and tax hikes continued to undermine the pound.

The pound retraced most of its losses the next day, as investors welcomed a surprise slowdown in UK inflation in December. Despite stoking speculation that the Bank of England (BoE) may cut interest rates in February, it could help ease the burden of government borrowing costs.

The UK’s latest GDP print reignited selling pressure on the pound on 16 January after falling short of economists’ forecasts. This was compounded by underwhelming UK retail sales figures on 17 January.

The pound hit a fresh five-month low against the euro the next day as recent economic data and dovish comments from a BoE official prompted investors to raise bets on further rate cuts.

The pound extended its multi-month low versus the euro on 21 January, leaving it a fraction above €1.18 amid growing BoE easing expectations. Meanwhile, the euro was buoyed by its strong negative correlation with the dollar after Donald Trump’s inauguration as President rocked the US currency.

The pound’s fortunes improved on 23 January after demand for the safer euro was knocked by a cautiously optimistic market mood, speculation of further ECB rate cuts and lacklustre Eurozone consumer confidence.

Having climbed into the €1.18 mid-range the previous day the pound leapt to within a whisker of the €1.19 benchmark on 24 January after the UK PMI showed lukewarm growth across British businesses edged up at the start of the year.

The pound nudged above the €1.19 benchmark on 27 January as optimism surrounding the government’s plans to stimulate growth overshadowed a pessimistic UK economic outlook from Morgan Stanley.

The pound firmed into the €1.19 mid-range on 29 January after UK Chancellor Rachel Reeves outlined government plans to make the UK the fastest-growing economy in the G7.

The euro was choppy the following day, initially softening after Eurozone GDP figures showed the bloc’s economy stalled in the fourth quarter before brushing off a widely expected rate cut from the ECB. Cautious forward guidance from the central bank pointed to a data-dependent approach to future decisions, limiting the single currency’s downside.

The pound euro rate ticked marginally higher on 31 January following the release of weak German inflation, jobs, and retail sales data that undermined the single currency. Meanwhile, the pound remained directionless amid an ongoing UK data lull.

The pound euro exchange rate ended the month at around €1.196

GBPEUR: 3-Month Chart

Looking ahead

The BoE is odds-on to make a 25-basis point cut on 6 February, which will likely be priced into the market, meaning it’s unlikely to have a significant impact on the pound. Investors will keep a close eye on the central bank’s forward guidance for clues about the possibility of future cuts.

Influential data from the UK economy in February: GDP (13 February), ILO Unemployment Rate (18 February), Consumer Price Index (19 February), Retail Sales (21 February), S&P Global/CIPS Composite PMI (25 February).