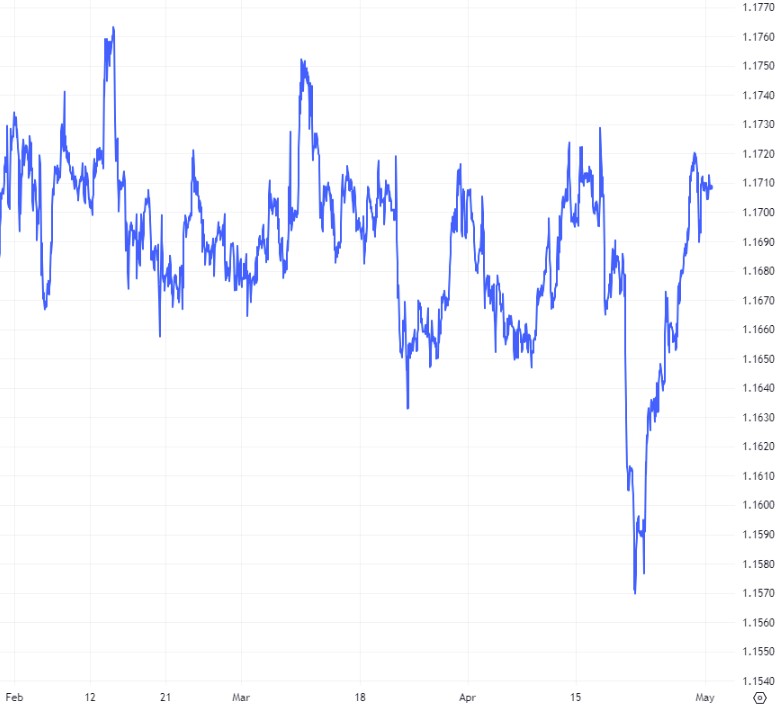

GBP-EUR Exchange rate recovers from 3-month low in April

The pound edged to within touching distance of 1.17 against the euro at the start of the month amid cooling German inflation and surprise UK manufacturing growth.

Activity for the manufacturing sector in March was revised up from 49.9 to 50.3, marking expansion for the first time since July 2022 and bolstering the UK’s economic outlook.

Inflationary easing in the Eurozone’s largest economy ramped up European Central Bank (ECB) interest rate cut bets, which sapped euro sentiment.

The pound euro exchange rate held steady on 3 April following the release of inflation data from the Eurozone.

Headline inflation eased from 2.6% to 2.4% rather than remaining static as forecast, while core inflation cooled from 3.1% to 2.9%, slightly below forecasts for a more modest drop to 3%.

As Eurozone inflation eases towards the ECB’s 2% target, speculation over upcoming interest rate cuts dented the single currency.

The pound continued to trade sideways the following day after mixed UK PMI data hit the headlines.

The finalised service sector reading printed at 53.1, down from 53.8 in February, and slightly below forecasts of a more modest fall to 53.4. Despite falling by more than expected, capping the pound’s potential, the sector remained firmly above the 50-point mark that signals growth.

The pound euro rate wavered near a ten-day low on 5 April amid surmounting rate cut expectations. A data lull in the UK left the pound exposed to expectations of a June interest rate cut from the Bank of England (BoE), with markets pricing in a total of four this year.

The ECB’s latest meeting minutes mirrored its recent dovish commentary, which supported investor expectations of a June interest rate cut in the Eurozone.

The single currency was further undermined by weaker-than-expected retail sales data, which printed at -0.5% for February, below expectations for a -0.4% reading and dropped sharply from January’s downwardly revised 0% stagnation.

Having drifted to a fourteen-day low against the euro in the 1.16 mid-range, the pound began firming following better-than-forecast UK retail data and anticipation of the ECB’s April policy meeting that soured the euro’s appeal.

The single currency slumped following the ECB’s latest interest rate decision on 11 April. As expected, the central bank kept rates on hold at 4.5% for a sixth consecutive time, but dovish remarks from the bank’s President Christine Lagarde dealt the euro a chastening blow.

This propelled the pound euro rate through the 1.17 barrier to touch a one-week high, before wavering the following day in the wake of weaker-than-forecast UK growth in February, which dampened investor interest in the UK currency.

The UK economy expanded by 0.1% in February, but the marginal uptick was below forecast. The print indicated ongoing economic fragility despite widespread optimism that the UK economy appears to be turning a corner after sliding into a technical recession last winter.

The pound euro rate was trapped in a narrow range in mid-April amid a flurry of notable data releases from the UK economy: underwhelming labour data showed that unemployment increased in February; a stickier-than-forecast inflation print forced investors to reevaluate the likelihood of imminent BoE interest rate cuts; and flatlining retail activity.

Dovish remarks by BoE deputy governor Dave Ramsden on 19 April caused the pound to slump to a three-month low against the euro. He said UK inflation could hold around its 2% target for the next three years, suggesting he does not need much more evidence of consumer prices cooling before voting for a rate cut. This sapped pound sentiment, pulling it to within a whisker of the 1.16 benchmark.

The pair began mounting a recovery on 23 April following hawkish comments from BoE Chief Economist Huw Pill, who said “In my view, against the background of a welcome decline in headline inflation, the outlook for UK monetary policy in the coming quarters has not changed substantially since the beginning of March.”

Investors interpreted this to mean that the central bank may still be some way off loosening monetary policy.

The pound was also underpinned by a better-than-expected services sector PMI index which rose from 53.1 to 54.9, beating market expectations of a more modest reading of 53.

The pound climbed into the 1.16 mid-range on 25 April as the euro faced headwinds amid an increasing appetite for risk that sullied appeal for the safe-haven currency.

The pound euro rate extended its gains on 29 April, breaking through the 1.17 benchmark amid a mixed German CPI reading that undermined the single currency. April’s preliminary year-on-year print came in slightly below forecasts, holding steady at 2.2% rather than warming to a predicted 2.3%. The month-on-month figure did warm, from 0.4% to 0.5% for April, but also missed a 0.6% prediction.

GBPEUR: 3-Month Chart

Looking ahead

All eyes will be on the BoE when it makes its next interest rate decision on 9 May. The central bank is widely expected to leave interest rates at a 15-year high of 5.25% again, before potentially firing the starting gun on its unwinding cycle in June if conditions are accommodative.

Influential data from the UK economy in May: Gross Domestic Product (10 May), ILO Unemployment Rate (14 May), Consumer Price Index (22 May), S&P Global/CIPS Composite PMI (23 May), Retail Sales (24 May).

With no monetary policy meeting scheduled in the Eurozone in May, inflation data on 17 May could signpost the potential timing of future policy loosening.